Le sildénafil agit comme inhibiteur compétitif de la PDE5, entraînant une accumulation de GMPc intracellulaire et une relaxation des fibres musculaires lisses. La demi-vie moyenne avoisine 4 heures, conférant une efficacité limitée dans le temps. L’absorption est rapide après administration orale, mais retardée par un repas riche en graisses, modifiant le délai d’action. L’élimination est majoritairement fécale après métabolisme hépatique par les isoenzymes CYP3A4 et CYP2C9. Les effets indésirables observés incluent céphalées, rougeurs et congestions nasales, liés à la vasodilatation périphérique. Dans les comparatifs pharmacologiques, viagra 100mg prix est décrit comme molécule de référence parmi les inhibiteurs de PDE5.

Microsoft word - 0302morn.doc

Goldman Sachs JBWere Goldman Sachs JBWere Pty Ltd Overseas Wrap Institutional Dealing Desk

Steve Maartensz [email protected] This communication has been prepared by the Sales and Trading Department and is not the product of the Investment Research Department.

Maket Statistics Chg Net 1d US 5 BEST & WORST PERFORMERS S&P 500 Goldman Sachs JBWere Overseas Wrap Stocks of Interest Strong: dept. stores; supercenters; internet retail; apparel; leisure products; general merch stores; specialty

stores; homefurnishing retail; life sciences tools and services; divsfd metals and mining

Weak: life and health insurance; divsfd banks; divsfd financial services; regional banks; multi-line insurance; tires

and rubber; consumer finance; independ. power producers; auto mfg.; healthcare equip

Citigroup agrees to exchange common stock for existing preferred shares; suspends dividends and

Preliminary fourth quarter GDP report shows economy contracted more than expected -- fastest rate

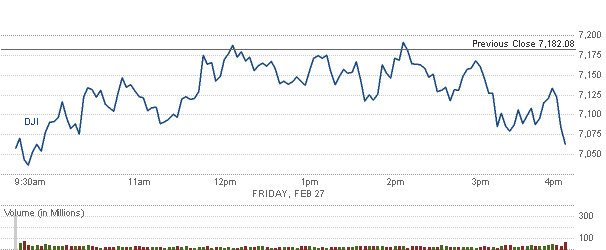

Stocks tumbled Friday and the S&P hit a 12-year low as news of the government's stake in Citigroup and General Electric slashing its dividend stirred worry in the market.

The Dow shed 119.15, or 1.7%, to close at 7,062.93. The Dow has now fallen for sixth straight months, losing 39% of its value. The last time it lost this much in a six- month period was in 1932.

The S&P 500 broke through its November low of about 740, dropping 2.4% to close at 735.09, its lowest close since December 1996. >> Dow Down 50% Since Peak Today's % 1 Week % MTD % YTD & Goldman Sachs JBWere Overseas Wrap NASDAQ 1377.84 S&P 500 735.09 CBOE VIX 46.35 FTSE CNBC 2950.77 Global 300 For the month, the Dow shed 12%, the S&P fell 11% and the Nasdaq lost 6.7%. The Dow's worst performers in February were, not surprisingly: Citigroup, Bank of America and General Electric. The best performers this month were Wal-Mart, IBM and Intel. The average bear market, over the past 100 years, has lasted 84 weeks. There are currently 10-12 weeks left in this market for it to become an average length recession.

US Market

U.S. stocks slid, sending the S&P 500 Index to a 12-year low, as the government cut shareholders’ stake in Citigroup. by 74% and the economy shrank at a faster pace than previously estimated.

Citigroup plunged 39% after the Treasury agreed to convert as much as $25 billion of preferred shares into common stock in a third rescue attempt.

Bank of America tumbled 25.75%, snapping a four-day rally in an S&P 500 group of banks. Alcoa and Boeing fell more than 3.8% after the Commerce Department said gross domestic product contracted at a 6.2% annual pace in the fourth quarter. The S&P 500 lost 2.4% to 735.09, its lowest close since December 1996. The Dow fell 119.15 points, or 1.7% to 7,062.93, leaving it 50% below its 2007 record and at its lowest level since May 1997. The S&P 500 slid 4.5% over the past five days, its third straight weekly decline, as companies from JPMorgan to Textron cut dividends to shore up capital and President Barack Obama proposed reducing payments to health-care companies. The index fell 11% in February amid concern Obama’s stimulus package won’t stem the deepening recession. Losses were limited today as investors snapped up shares after the S&P 500’s valuation slid to a 23-year low. Citigroup sank 39.02% to $1.50, an 18-year low. The Treasury Department said it will swap its preferred shares for common stock only if private holders agree to the same terms. The U.S. doesn’t immediately intend to inject additional money after channeling $45 billion to the company last year.

More than 1.8 billion shares of Citigroup changed hands today, setting a record for trading volume for a U.S. stock, according to the New York Stock Exchange. Citigroup accounted for about 13% of total trading volume of 14 billion shares, which was 46% more than the three-month daily average of stocks traded on all U.S. exchanges.

Goldman Sachs JBWere Overseas Wrap Bank of America, which also got $45 billion from the government, dropped 25.75% to $3.95. Wells Fargo a recipient of $25 billion in U.S. funds, slumped 16% to $12.10.

The companies are among more than 400 financial institutions that received cash in exchange for preferred shares from the government.

The U.S. government has pledged more than $11.6 trillion in the past 19 months on behalf of American taxpayers to bail out banks and stimulate economic growth.

It hasn’t been enough to stop banks from collapsing. Regulators seized 14 lenders this year, including eight this month. Last year, regulators shuttered 25 banks, including Washington Mutual I., the biggest bank failure in U.S. history.

The 10% decline in the S&P 500 Banks Index halted a four-day advance, 30% advance in the measure that was spurred by decreased concern that banks would be nationalized and a request for additional bailout funds for the industry in Obama’s first budget proposal.

Weighting Dwindles

Financial companies may fall to 7% of the S&P 500 before losses in bank stocks end, extending a drop that already cut the weighting in half

Citigroup, which had a market value of $277 billion at the end of 2006, has tumbled 97% since then, leaving it valued at $8.2 billion.

General Electric retreated 6.5% to $8.51. The company, whose finance unit has been battered by rising loan losses, cut its annual dividend for the first time since at least 1940 as Chief Executive Officer Jeffrey Immelt moves to preserve cash and protect the company’s top AAA credit rating. The quarterly payout was lowered to 10 cents a share from 31 cents. S&P: GE outlook still negative after dividend cut. Standard & Poor's on Friday said its outlook on General Electric Co remains negative after the conglomerate said it plans to reduce its quarterly dividend from 31 cents to 10 cents, preserving about $9 billion a year. Though the dividend cut will give GE more discretionary cash flow from its industrial operations than anticipated, the economic outlook has deteriorated since the negative outlook was assigned in December, S&P said in a statement. S&P rates GE "AAA," the highest possible investment-grade rating. A negative outlook typically indicates a rating cut is likely within two years. MetLife Tumbles MetLife Inc. fell the most since October, tumbling 23% to $18.46. S&P downgraded the biggest U.S. life insurer and nine other companies in the industry on the prospect of further investment losses. A measure of insurers in the U.S. stock benchmark sank 7.9%.

Crude oil fell 1.02% to $44.76 for the first time in four days, pushing shares of Exxon

The S&P 500 traded for as little as 12.8 times company profits from the past 10 years. That was the cheapest valuation since February 1986 Goldman Sachs JBWere Overseas Wrap Dell Inc. had the biggest gain in almost a month, climbing 3.9% to $8.53. The second-largest maker of personal

computers reported fourth-quarter profit that topped analysts’ estimates and said it will save an additional $1 billion a year by 2011. Blackstone 26% to $4.87 for the steepest advance since November. Chairman Stephen Schwarzman reassured investors during a conference call that Blackstone, the world’s biggest private-equity firm, has the ability to protect its existing holdings and invest in new deals.

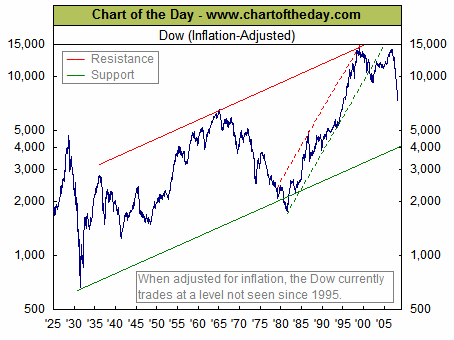

Chart of the Day - For some long-term perspective, today's chart illustrates the Dow adjusted for inflation since 1925. There are several points of interest. For one, the inflation-adjusted Dow has gained a mere 55% since its 1929 peak and gained only 10% since its 1966 peak – not that impressive considering it took many decades to achieve those gains. It is also interesting to note that based on an inflation-adjusted Dow, the current bear market actually began in 1999 only to be interrupted briefly by a multi-trillion dollar credit bubble. That bubble has burst, of course, and the Dow now trades at a level not seen since 1995. Goldman Sachs JBWere Overseas Wrap

US Banks/InvestBanks

The U.S. government ratcheted up its effort to save Citigroup., agreeing to a third rescue attempt that will cut existing shareholders’ stake in the company by 74%. The Treasury Department said it would convert as much as $25 billion of preferred shares into common stock provided private holders agree to the same terms, the government said in a statement today. The conversion would give the U.S. a 36% stake in the New York-based company. Under the terms of the deal, Citi will exchange common stock for as much as $27.5 billion of its preferred securities at a conversion price of $3.25 a share.

Existing shareholders will see their ownership of the bank fall as low as 26 percent.

The government stake is now close to 8%.

UK/European Banks

Lloyds fell 22% after saying it hadn’t reached agreement on a government asset insurance program and reporting a record loss at its HBOS unit. Talks with the U.K. Treasury are “progressing and well advanced,” the bank said in a statement today. Lloyds rose 30% Thursday on speculation it would follow Royal Bank into the asset protection program, which agreed to insure 325 billion pounds of investments for the Edinburgh-based lender. HBOS posted 9.9 billion pounds of loan losses and writedowns last year, up from 2 billion pounds in 2007.

Goldman Sachs JBWere Overseas Wrap Weekly Wrap

Financials remained in focus for another week, as the U.S. government now owns 36% of the common stock of Citigroup (C), the Obama administration unveiled its Capital Assessment Program, which includes stress tests for the 19 largest domestic banks, and economic data showed continued deterioration. But while the larger banks were under pressure yet again, the financial sector as a whole advanced 2.0% this week. That cannot be said for the rest of the market, as an 11.4% plunge in Health Care and an 8.3% decline in Industrials helped the S&P join the Dow at new 11-year lows; 734.52 and 7033.62, respectively. Overall, the S&P lost 4.5% this week, the Dow lost 4.1%, the Nasdaq lost 4.4% and the Russell lost 5.3%.

On Monday, the major averages looked to open the week on a strong note. Strength in financials, specifically Citi, led to a higher open on reports the government may convert its preferred shares in the financial services giant into common shares. It would own no more than a 40% stake, which helped ease the prior sesssion's nationalisation fears.

However, the stock market trended downwards throughout the session, eventually closing sharply lower. The managed care group plunged after the Center for Medicare & Medicaid Services released its preliminary 2010 Medicare Advantage Rates, showing a capitation rate increase of only 0.5%, well below Street expectations. Financial sector fears also remained in focus despite the Citi reports, helping the sector lose gains of as much as 4.6% to close 3.0% lower.

The stock market rebounded on Tuesday, despite a piece of disappointing housing data. The S&P/CaseShiller House Price Index showed a year-over-year decline of 18.6%, larger than the -18.3% consensus estimate.

The big corporate development of the day came from JPMorgan (JPM), who reduced its dividend to $0.05 from $0.38 to retain $5 billion in additional common equity per year, while also saying first quarter performance to date has been "solidly profitable", even after "significant" additions to reserves, and roughly in line with analyst expectations. Shares of JPM rallied 7.7% that day.

Tuesday also was the beginning of Federal Reserve Chairman Ben Bernanke's Semiannual Monetary Policy Report before Congress. He told the Senate Banking Committee that day that there is "considerable economic uncertainty," but the recession may end in 2009 and the economy may recover in 2010.

Wednesday proved to be a volatile day, as the major averages resumed their downward trend in the morning before rebounding in the early afternoon after the Obama administration announced its Capital Assessment Program, only to roll over in the last 20 minutes of the session.

A second piece of disappointing housing data contributed to the downward move in the morning. Existing Home Sales slipped 5.3% in January to an annualized rate of 4.49 million units. That compared negatively to the consensus estimate of 4.79 million units and is the lowest level since 1997.

But the market rebounded temporarily in the afternoon after the CAP announcement. The terms state that capital provided will be in the form of a preferred security that is convertible into common equity at a 10% discount to the price prevailing prior to February 9. That capital will be provided to banks who undergo a stress test that says they need those funds to perform their duties in the financial system.

Thursday proved to be a similar session to Monday, as the market opened higher only to trend lower throughout the day. It was initially supported by a rally in Europe, specifically UK banks, after the government there unveiled its long awaited asset protection scheme. But bleak economic data and another plunge in managed health care stocks did little to support the rally, and the market eventually turned lower.

Durable Goods Orders ex-transportation dropped a larger-than-expected 2.5% in January, more than the -2.2% consensus estimate, while the prior month was revised sharply lower to -5.5% from -3.6%. The market also received its third consecutive piece of disappointing housing data as New Home Sales dropped to an annualized rate of 309,000 units in January. That was below the 324,000 consensus estimate, 48.2% below the year-ago level and marked a new low for records dating back to 1963.

Meanwhile, managed health care names came under pressure for a second time this week after President Obama announced he will cut Medicare spending as part of his health care plan.

That brings us to Friday’s session, which proved to be no better than Thursday. The S&P and Dow set those 11-year lows this morning on heavy pressure in the financial sector after Citi surprisingly suspended dividends on its preferred

Goldman Sachs JBWere Overseas Wrap shares and announced a $9.6 bln fourth quarter goodwill impairment, all while confirming the government would convert its preferred shares in the company to common stock.

What's more, fourth quarter GDP was revised sharply lower, to -6.2% from the Advanced reading of -3.8%, which was well below the -5.4% consensus estimate. The decrease primarily reflected negative contributions from exports, personal consumption expenditures, equipment and software, and residential fixed investment (i.e. most of the major components). While this data is essentially old news, seeing that we're two-thirds of the way through the first quarter, it still resonates as a startling reminder of how quickly things turned. Unfortunately, the current trends don't paint a much better picture.

One corporate headline from the afternoon, as General Electric (GE) cut its long-standing dividend to $0.10 from $0.31 to save nearly $8.9 bln a year. Shares of GE initially rallied on the news, but a reduction at this juncture -- it doesn't kick in until the third quarter of 2009 -- will feed into concerns that there won't be a quick recovery for GE, or the global economy, given its multinational presence.

The Economic Calendar is extremely light next week, that is until Friday when the Bureau of Labor Statistics releases the highly-anticipated Change in Nonfarm Payrolls figure for February.

Started Week Ended Week S&P 500 Russell 2000 EUROPEAN MARKETS

Last Trade OTHER NEWS -WSJ: FDIC Poised to Double Fees Charged to Lenders. Federal regulators are expected to raise the fees that they charge banks by more than double in an effort to replenish the government's deposit-insurance fund, said people familiar with the matter. The move represents a clash of two competing interests. It would protect consumers by bolstering the fund that insures their deposits in the event of a bank failure. At the same time, some government officials worry that banks are too fragile to shoulder the additional cost. WSJ: Red Ink Clouds Role of Fannie, Freddie. Red ink is starting to gush in even larger quantities at Fannie Mae and Freddie Mac, as the government wrestles with deciding what role should be played by the two biggest providers of funding for U.S. home mortgages. Fannie late Thursday reported a $25.2 billion loss for the fourth quarter, and Freddie is expected to report a huge loss for the latest quarter when it posts earnings, probably in early March. Homeowner defaults have continued to increase even as the government has redirected the two companies to focus their attention on preventing foreclosures and propping up the housing market. US Energy Secretary Chu: OPEC oil decision needs to help global economy. "We are very focused on restoring U.S. and global economic growth, and expect OPEC members to take appropriate consideration of the current global economic situation in their discussions," a department spokeswoman told Reuters. OPEC ministers meet in Vienna on March 15 to decide whether another round of oil production cuts are needed to help keep crude prices from falling. "We believe a transparent oil market with stable energy prices and a secure supply of oil is the best policy in the current economic situation," said the department spokeswoman, who added Chu will be speaking with energy ministers from both oil producing and consuming countries about the state of the global economy US ECRI weekly leading economic index drops to 105.6 from 107.2 – weakest since April 1995. The Economic Cycle Research Institute, a New York-based independent forecasting group, said its Weekly Leading Index dipped to 105.6 for the week ending Feb. 20 from 107.2 in the previous week. It was the lowest the index has been since April 21, 1995, when it read 105.6. The annualized growth rate was steady at negative 24.1 percent, according to the weekly report. "The WLI has dropped to a new cycle low, clearly indicating that the recession will intensify in coming months, with no recovery in sight," said Lakshman Achuthan, Managing Director at ECRI. Goldman Sachs JBWere Overseas Wrap •

FED SPEAK -Philadelphia FED Plosser: Fed should switch other assets for Treasuries. "The current crisis and the Fed's interventions have dramatically altered the composition of the assets on our balance sheet and created confusion in the minds of many as to the respective roles of the central bank and the fiscal authority," Plosser said. An agreement with the Treasury to switch U.S. government bonds for these less-liquid non-traditional assets on the Fed's balance sheet would help the central bank focus on conducting traditional monetary policy. "With Treasuries back on the balance sheet, the Fed will be able to drain reserves in a timely fashion with minimal concerns about disrupting particular credit allocations or the pressures from special interests," said Plosser, who is not a voting member on the Fed's policy-setting committee this year. He said such an agreement would transfer funding of the credit programs to the Treasury, "thus ensuring that credit policies that place taxpayer funds at risks are under oversight of the fiscal authority. "Second, it would return control of the Fed's balance sheet to the Fed, so that we can continue to conduct independent monetary policy," he said. Longer-term assets, such as agency MBS, "may prove difficult to sell for an extended period of time if markets are viewed as 'fragile' or specific interest groups are strongly opposed," he said, adding that this could lead to inflation down the road. "We must ensure that our current credit policies do not constrain our ability to conduct appropriate monetary policy in the future," Plosser said. He said the "jury is still out" as to how effective these so-called credit easing policies will be. Plosser reiterated his call for an explicit inflation target and said the Fed should publicly commit to achieving that target over an intermediate time horizon. "Such a commitment would help anchor expectations more firmly and diminish concerns of persistent inflation or persistent deflation -- not an inconsequential issue in the current environment," he said. Plosser said the lack of clear ground rules can lead to markets speculating on what the next asset class or company the Fed will rescue. This is counterproductive and can lead to increased market volatility, he warned. Boston FED Rosengren: Financial stability key to recovery. "We need to be sure that actions to support the stability of the financial system are taken without delay," Eric Rosengren, president of the Boston Federal Reserve Bank, said in remarks prepared for a monetary policy forum in New York. At the University of Chicago Booth School of Business/ Brandeis International Business School forum, Rosengren said the U.S. economy is "likely to shrink significantly" in the first half of this year. "The added clarity on the long-run intentions of monetary policy . might keep inflation expectations well anchored and real interest rates low enough to help get the economy moving again," the policy-maker said. "The largest components of the expansion . are likely to become unappealing to market participants as financial conditions improve and interest rate spreads decline," he said. Rosengren said the various Fed programs to reduce the cost of credit to a variety of borrowers would be more successful in turning the economy around than the "quantitative easing" pursued by Japan during the 1990s. "Increasing reserves when financial intermediaries are capital-constrained," the theory behind Japan's policies, "is unlikely to have much impact," Rosengren said.

San Francisco Fed Yellen: Long-run inflation forecasts useful. "The FOMC's recently released longer-run inflation projections should be useful in this regard, helping to reinforce inflation expectations of around 2 percent," Yellen said in remarks at forum in New York. Yellen discussed a paper on oil prices and the conduct of Fed policy at the University of Chicago Booth School of Business/Brandeis International Business School monetary policy forum. "There was little evidence that (Fed) policy was inappropriate" in recent years as oil prices roared to record levels and headline inflation jumped, Yellen said. Wage growth stayed well contained and inflation persistence appeared to be low during that time, "most likely because of increased Fed credibility," she said. "My hope is that inflationary expectations will remain similarly well-anchored now, serving to stabilize core inflation." St. Louis FED Bullard: Expects oil prices higher over time. "I would expect oil prices to go up over time because of the finiteness of the resource," he said at a conference organized by the University of Chicago Booth School of Business and Brandeis International Business School. "It seems plausible to me that you could have longer-run trend- line behavior in particular prices." Paper argues FED erred in ignoring oil price rise. "The Fed was a bit too eager to dismiss the trend-like rise in oil prices as it continued into 2005 and 2006," says the study by two economists and two academics and presented at a conference by the University of Chicago Booth School of Business and Brandeis University. "It seems the Fed was relying too much on its anti-inflation credibility and not enough on actual policy tightening," the study says. Oil prices rose from around $20 a barrel in 2001 to more than $140 a barrel in mid-2008. The study was prepared by Ethan Harris of Barclays Capital, Bruce Kasman of JPMorgan Chase, Matthew Shapiro of the University of Michigan and Kenneth West of the University of Wisconsin. "The Fed stuck to its 'measured pace' tightening in the face of persistently high headline inflation, the signs of 'froth' across the capital markets and the housing markets and the persistent increase in oil and other commodity prices," they wrote. The authors said the Fed erred in focusing single-mindedly on measures of inflation that strip out volatile food and energy costs, known as "core" inflation, the study says. The U.S. central bank was regularly on the defensive regarding this practice, said the authors. "Oil prices and upward pressure on inflation expectations ended up becoming a sideshow in 2008 and for policy decisions for the foreseeable future," the authors said. Goldman Sachs JBWere Overseas Wrap US ECONOMIC DATA – The U.S. economy shrank in the fourth quarter at a faster pace than previously estimated as consumer spending plunged, companies cut inventories and exports sank. Gross domestic product contracted at a 6.2% annual pace from October through December, more than the -5.4% economists anticipated and the most since 1982, according to revised figures Consumer spending, which comprises about 70% of the economy, declined at the fastest pace in almost three decades. The 2.4% revision( Previously reported as -3.8%) was almost five times as large as the average adjustment. For all of 2008, the economy expanded 1.1% as exports and government tax rebates in the first six months helped offset the deepening slump in consumer spending that followed. Consumer spending dropped at a 4.3% annual rate last quarter, the most since 1980, after falling at a 3.8% pace the previous three months. That marks the first time purchases have dropped by more than 3% in consecutive quarters since record-keeping began in 1947. Companies trimmed inventories at a $19.9 billion annual rate last quarter rather than allowing them to swell at a $6.2 billion pace as previously reported. The updated reading accounted for half of the 2.4% reduction in growth. Purchases of new equipment also plunged last quarter. Business investment dropped at a 21% pace, the most since 1980. Spending on equipment and software dropped at a 29% pace, the most since 1958. The collapse in global trade subtracted a half percentage point from growth last quarter, compared with the 0.1%gain projected in the advance report. . U.S. business activity contracted in February for a fifth consecutive month, a sign manufacturing is weakening as the recession extends into a second year. The Institute for Supply Management-Chicago Inc. said its business barometer increased to 34.2, higher than the 33 forecast, from 33.3 the prior month, when it reached the lowest reading since March 1982. The new orders gauge decreased to 30.6 from 30.7 the previous month and the production index improved to 34.7 from 29.7. The employment index slumped to 25.2, the lowest level in seven years, from 34.8, the report showed. A measure of prices paid for raw materials decreased to 37.8 from 39.8 the prior month, while a gauge of delivery times fell to 51 from 51.9. Economists watch the Chicago index for an early reading on the outlook for overall U.S. manufacturing, which makes up about 12% of the economy. Confidence among U.S. consumers fell in February, weighed down by job losses, declining stock prices and plunging home values. The Reuters/University of Michigan final index of consumer sentiment fell for the first time in three months to 56.3( Versus expectations of 56) from 61.2 in January. The gauge reached a 28-year low of 55.3 in November. The group’s preliminary report earlier this month showed a sentiment reading of 56.2. The University of Michigan’s index of consumer expectations six months from now, which more closely predicts the direction of consumer spending, fell to 50.5, from 57.8 in January. Goldman Sachs JBWere Overseas Wrap A measure of current conditions, which reflects Americans’ perceptions of their financial situation and whether it’s a good time to buy expensive items such as cars, fell to 65.5 from 66.5. Inflation Expectations -Consumers projected an inflation rate of 1.9% over the next 12 months, compared with 2.2% in the January survey. Over the next five years, Americans expected a 3.1% rate of inflation, compared with the 2.9% forecast last month. These figures are tracked by Federal Reserve policy makers.

US DOLLAR -The dollar rose to the highest in almost three years against the currencies of six major U.S. trading partners as the deepening recession and the third government bailout of Citigroup stoked demand for safety. The pound touched a one-week low against the dollar as consumer confidence in the U.K. held near the weakest in 30 years. The Hungarian forint and Polish zloty rose against the euro on speculation international aid will bolster Eastern Europe’s banking system. The dollar gained to $1.2663 per euro from $1.2744 yesterday. The U.S. currency decreased 1 percent to 97.54 yen from 98.52. The euro dropped 1.6 percent to 123.52 yen from 125.52. The Dollar Index, which the ICE uses to track the U.S currency versus the euro, yen, pound, Swiss franc, Canadian dollar and Swedish krona, reached 88.490, the highest level since April 2006. The Aussie traded at .6390, down 75 basis points.

Main Points 1) Stocks Drop to Multiyear Lows in High Volume -The government is taking a major stake in Citigroup, GE is slashing its dividend, and fourth quarter GDP readings show the economy contracted at its sharpest rate since 1982. Those headlines led to some very choppy trading and pushed the S&P 500 and the Dow to their lowest intraday and closing levels since 1997.

A rather bearish close to the prior session, in which the stock market declined roughly 1.6%, left market participants in a dour mood. The pessimistic tone was exacerbated when Citigroup (C 1.50, -0.96) announced it is offering common shares for up to $27.5 billion in existing preferred equity. The government will exchange a maximum of $25 billion face value of its preferred stock, which gives the government a 36% stake in the company.

Reports earlier in the week indicated the government was in talks with Citigroup, so the announcement wasn't a total surprise. However, news that Citi is suspending dividends on common shares and its preferred shares came as a real disappointment.

Though the transaction is expected to increase Citigroup's tangible common equity, which will help it absorb future losses, Standard & Poor's revised its outlook for Citi to Negative. Moody's lowered Citi's long-term ratings.

Economic bellwether General Electric (GE 8.51, -39.02%) slashed its quarterly dividend to $0.10 per share from $0.31 per share. The dividend cut is expected to save the company some $9 billion annually, according to reports. The cut will also help protect GE's AAA credit rating.

Analysts were anticipating the dividend cut, given the troubles and challenges facing GE's capital unit. Because of the unit's exposure to capital markets the stock has traded similar to financial stocks even though the company is an industrial stock.

In turn, GE's weakness caused the industrial sector to fall 2.7% this session, but 18.0% this month. Financial stocks dropped 7.4% this session, and 18.4% in February. They weren't alone; all 10 sectors in the S&P 500 finished lower for the session and for the month.

Broad-based selling pushed all three major indices lower for the session. The S&P 500 closed near its worst levels of the session.

Economic data remains gloomy. Fourth quarter GDP was revised lower to reflect an annual rate of -6.2% versus a previously estimated -3.8%. The decrease in fourth quarter activity primarily reflected negative contributions from

Goldman Sachs JBWere Overseas Wrap exports, personal consumption expenditures, equipment and software, and residential fixed investment. To little surprise, government spending provided a positive contribution.

A consistent flow of negative headlines has left pessimism largely unchecked as traders continue to bet against stocks. The bet seems to have paid off for bearish traders since February marked the worst monthly performance for each of the major indices since October.

More than 2 billion shares traded hands on the NYSE this session. That's the most since December.

2) GOLD Gold fell, capping the first weekly loss in three, as the dollar strengthened to the highest level since April 2006, eroding the appeal as an alternative investment. The U.S. Dollar Index rose against the currencies of six major trading partners on demand for a haven after the U.S. bailed out Citigroup for a third time, stoking concerns that the credit crisis and the recession may deepen. Gold futures for April delivery fell $3.85 or .41% to $942.45 an ounce .That left the Gold down 5.1% for the week, the first decline since Feb. 6 and the biggest since Dec. 5. The Philly Gold index fell .63%. 3) BASE METALS- Copper fell, snapping four days of gains, on renewed concern demand will drop as fresh data showed the global recession is deepening. The U.S. economy shrank in the fourth quarter at the steepest rate since 1982. Consumer spending fell at the fastest pace in almost 30 years. Japan’s manufacturers cut production by a record last month and economic growth slowed in India and Malaysia last quarter. The revised 6.2% drop in U.S. gross domestic product, on an annual basis, took analysts by surprise. The median projection of 74 economists was 5.4%. Consumer spending tumbled at a 4.3% annual pace last quarter, the sharpest rate of decline since 1980, after falling at a 3.8% rate the previous three months. That marks the first back-to-back decreases of more than 3% since record- keeping began in 1947. LME SPOT METAL PRICES 4) OIL -Crude oil fell for the first time in four days on concern energy demand will decline, after the U.S. economy contracted faster than anticipated. Oil dropped after the government said gross domestic product shrank at an annual pace of 6.2% in the fourth quarter, the most since 1982. Demand has cratered, and after these numbers we can expect it to sink further. The dollar is up, taking additional froth out of the market Crude oil for April delivery fell 46 cents, or 1% to settle at $44.76 a barrel . Prices are up 7.4% for the month and 0.4% so far this year. Futures have dropped 70% from the record $147.27 a barrel reached on July 11. Also, Japan’s 10% drop month-on-month decline in factory output exceeded the December record drop of 9.8%, the Trade Ministry said today in Tokyo. Household spending fell 5.9% from a year earlier, the biggest drop in more than two years. The U.S. and Japan are responsible for about 30% of global oil consumption. 5) US BONDS - Treasuries posted a weekly loss, the biggest for longer-term securities in a month, on concern debt supply will swell to unprecedented levels as the U.S. borrows to fuel economic growth and finance a $1.75 trillion budget deficit. Securities due in 10 years or more fell Friday on concern a Federal Deposit Insurance Corp. move to expand bank- debt guarantees will add more supply to the market. Notes due in seven years or less rose as the economy shrank more than forecast and the U.S. announced a third rescue effort for Citigroup Inc. The gap between two- and 10-year note yields was the widest in three months. Treasuries lost investors 0.4% in February after a 3.1% decrease in January that was the most in almost five Years. A 3.5% decline so far last year compares with a 1.9% gain for the same period in 2008. The FDIC, in an expansion of its Temporary Liquidity Guarantee Program, approved an interim rule to back new debt sold by banks that would later convert into common shares. The backing will be available to senior unsecured debt that converts into shares no later than the guarantee’s expiration, which can last through June 30, 2012. 6) LIBOR -The London interbank offered rate, or Libor, that banks say they charge each other for overnight loans in dollars rose to the highest level in almost three months, according to the British Bankers’ Association. The rate increased eight basis points to 0.36%, the highest level since Dec. 4, the BBA said. The three-month rate was little changed at 1.26% 7) THE WEEK AHEAD -Earnings reporting season slows markedly in the coming week. While quite a few companies are listed on the Earnings Calendar, most are not big names. Goldman Sachs JBWere Overseas Wrap AIG (AIG) is sure to be in the news. Media reports have suggested the company could announce a quarterly loss in the neighborhood of $60 billion on Monday, although the exact date of AIG's earnings release has not been confirmed.

The Senate Banking Committee has scheduled a hearing Thursday to examine government aid to the insurer. Treasury Secretary Geithner will be testifying the same day on the U.S. Treasury budget.

The Economic Calendar, which contains a large number of important releases, is highlighted by Friday's release of the February employment report. In a continuation of discouraging trends, nonfarm payrolls are expected to show 615,000 jobs were lost in February. Additionally, retailers will report their February same-store sales Thursday.

Monday, March 2:

• Earnings: DISH Network (DISH), Edison Intl (EIX), McDermott (MDR) • Economic Data: Personal Income and Spending (Jan.). Construction Spending (Jan.). ISM Index (Feb.) • Events: Genentech Investment Community Meeting (9:00 ET) • Conferences: Citi 2009 Global Property CEO Conference (Day 2 of 4). Deutsche Bank Securities Media and

Telecommunications Conference (Day 1 of 3). Morgan Stanley Technology Conference (Day 1 of 3)

Speakers: Boston Fed President Rosengren speaks on the credit crisis and financial regulation (11:30

ET). Richmond Fed President Lacker speaks on government lending and monetary policy (12:45 ET)

Tuesday, March 3:

• Earnings: AutoZone (AZO), MBIA (MBI) • Economic Data: Pending Home Sales (Jan.). Auto Sales (Feb.) • Events: None • Conferences: Citi 2009 Global Property CEO Conference (Day 3 of 4). Deutsche Bank Media and

Telecommunications Conference (Day 2 of 3). Merrill Lynch Healthcare Products and Services Conference (Day 1 of 3). Morgan Stanley Technology Conference (Day 2 of 3)

Speakers: Atlanta Fed President Lockhart speaks on U.S. economy, role of the Fed (8:00 ET)

Wednesday, March 4:

• Earnings: Big Lots (BIG), BJ's Wholesale (BJ), Costco (COST), Toll Brothers (TOLL), Foot Locker (FL), PetSmart (PETM)

• Economic Data: ADP Employment Change (Feb.). ISM Services (Feb.) • Events: Weekly Crude Inventories (week ended Feb. 28). Fed releases Beige Book (14:00 ET) • Conferences: Citi 2009 Global Property CEO Conference (Day 4 of 4). Deutsche Bank Media and

Telecommunications Conference (Day 3 of 3). Keefe, Bruyette & Woods Regional Bank Conference (Day 1 of 2). Merrill Lynch Healthcare Products and Services Conference (Day 2 of 3). Morgan Stanley Technology Conference (Day 3 of 3)

Speakers: Dallas Fed President Fisher speaks at TCU (8:30 ET). Atlanta Fed President Lockhart

speaks on U.S. economic outlook (12:00 ET)

Thursday, March 5:

• Earnings: Urban Outfitters (URBN), Marvell Technology (MRVL) • Economic Data: Productivity-Revised (Q4). Initial Claims (week ended Feb. 28). Factory Orders (Jan.) • Events: Treasury Secretary Geithner testifies at hearing on U.S. Treasury budget (10:00 ET). Senate

Banking Committee hearing on government aid to AIG. Retailers report same-store sales

• Conferences: Deutsche Bank Hospitality & Gaming Conference (Day 1 of 5). Keefe, Bruyette & Woods

Regional Bank Conference (Day 2 of 2). Merrill Lynch Healthcare Products and Services Conference (Day 3 of 3)

Speakers: Atlanta Fed President Lockhart speaks on U.S. economy (12:45 ET)

Friday, March 6:

• Earnings: H&R Block (HRB) • Economic Data: Employment Report (Feb.). Consumer Credit (Jan.) Goldman Sachs JBWere Overseas Wrap

• Events: None • Conferences: Deutsche Bank Hospitality & Gaming Conference (Day 2 of 5) • Fed

Trader Talk

1) The Citi story is a nightmare that keeps getting worse, with no end in sight. The fact that it’s occurring on a day when we’re getting horrible GDP numbers adds some kerosene to the mix.

2) The fear is that this will happen to all the preferreds that the government has given to the banks. In one word, it’s dilution. Points of Interest

ADR's & OVERSEAS STOCKS Last_Price Chg Net 1d

RESOURCES -The Baltic Dry Index, a measure of shipping costs for commodities, had its first weekly drop in almost two months on reduced demand for so-called capesize vessels to haul iron ore for making steel. Rio said Feb. 23 it may delay cargoes after rains flooded railways linking mines to ports The index fell 113 points, or 5.4%, to 1,986 points last week, according to the Baltic Exchange, the first such decline since the week ended Jan. 2. In the UK - Rio Tinto Plc fell 3.9% to 18.01, after being down 6.5%. The stock fell .49% for the week (A$ 40.35, a 14.6% DISCOUNT to A$ CLOSE of $47.25). Vol 6.37m versus a month avg of 10.3m.

Goldman’s downgraded the stock to “sell” from “neutral,” after the bank reduced forecasts for prices of industrial metals. Kazakhmys Plc declined 16.75 pence, or 6% to 261.5 after Goldman’s cut its rating for the copper producer to “neutral” from “buy.” NB RIO rose 2.05% in Aussie on Friday .

ElseWhere BHP Billiton Plc fell 4.24%, after being down 7.6%. The stock fell 4% for the week. (A$24.78 a 14.04% discount to $A close of $28.83) - Vol 15.5m versus a 3 month avg of 24.9m . Elsewhere Anglo fell 2.44%, whilst Xstrata rallied +6.3% NB BHP rose .80% in Aussie on Friday BHP ADRS closed at $28.50 versus the Aussie close of $28.83 (-1.16%) Range =$27.53 -$2934 VWAP =$28.62. NB If the move is reflected in Aussie, it will take approx 5.2 pts off the ASX 200. Goldman Sachs JBWere Overseas Wrap US RESOURCES –Alcoa fell 4.3% , whilst Freeport rallied +1.1% AWC – ADRS trading at $1.193 Versus the Aussie close of $1.205 EQN – in Canada trading at $1.78 Versus the Aussie close of $1.81. Vol 7.3m versus 22.7m on Thursday & an avg of 2.68m LGL –ADRS trading at $A3.35 Versus the Aussie close of $3.30 PDN – In Canada trading at $2.982 versus the Aussie close of $3.00 CWN- US Gaming stocks under pressure (Percentage Change) Last 1

MCC/FLX – US Coal stocks mixed. Coal:

. JHX/BLD – US Homebuilders/building stocks under pressure Homebuilders: BSL – US Steel stocks struggled, finishing the week down 15.7% Goldman Sachs JBWere Overseas Wrap

IPL- US Peers mixed Fertilizers:

Mosaic Co., the world’s largest maker of phosphate crop nutrients, rose on speculation that Cargill Inc., its largest shareholder, may take the fertilizer company private. Speculation of a move by Cargill, the largest privately held U.S. company, follows an all-stock bid by CF Industries Holdings Inc. for rival fertilizer maker Terra Industries Inc. and Agrium Inc.’s stock-and-cash proposal to purchase CF. Cargill, which owns about 64% of Mosaic, agreed in 2004 to freeze its stake following Mosaic’s creation from the combination of IMC Global Inc. and Cargill’s crop-nutrition business. That standstill agreement ended Oct. 22. UK Market

U.K. stocks fell for the first time in three days, led by banks after Lloyds said it hadn’t reached an agreement on its participation in the government’s asset insurance program. Lloyds, which also reported a drop in full-year earnings, slumped 22%, paring some of yesterday’s 31% advance. Royal Bank of Scotland and Barclays Plc lost at least 17%. AstraZeneca Plc fell on reports the company “buried” unfavourable studies about its antipsychotic drug Seroquel and after President Barack Obama said generic-drug makers should be allowed to sell cheaper medicines in the U.S. The FTSE 100 Index dropped 85.55, or 2.2% to 3,830.09 in London. Commodity producers and insurance companies also retreated, extending this month’s sell off to 7.7% Indexes extended declines after the U.S. Treasury cut shareholders’ stake in Citigroup Inc. by 74% and a report showed the U.S. economy shrank at a faster pace than previously estimated. Lloyds declined 22% to 58.3 pence. The biggest U.K. banks by customers said talks with the government were “progressing”, but the Treasury said an announcement wasn’t expected today. The lender reported a 75% drop in full-year profit to 819 million pounds and said it expects to report a loss for 2009 as writedowns and loan impairments increase. The bank’s HBOS Plc unit posted a 2008 loss of 7.5 billion pounds after bad loans at its corporate lending arm rose. Banks shares rallied yesterday after RBS said it will put 325 billion pounds of investments into a state insurance program and shift toxic assets to a new unit. Barclays, the U.K.’s third biggest lender, fell 17% to 93.4 pence. RBS, the largest bank controlled by the government, dropped 20% to 23.2 pence. AstraZeneca declined 4.8% to 2,243 pence. The drugmaker failed to publicize results of at least three clinical trials of Seroquel, a company official said in an internal 1999 e-mail unsealed as part of litigation over the medicine. The shares also fell after President Obama yesterday proposed spending $634 billion to expand U.S. health care while spending less government money for some drugmakers and health insurers. He announced, under the proposed budget, that copies of costly biotechnology medicines would be allowed in the U.S. with few delays. Eli Lilly & Co. of the U.S. and AstraZeneca said they would lose “several hundred million” dollars each in drug sales if the health-care plan was approved. Goldman Sachs JBWere Overseas Wrap Marks & Spencer Group declined 3.5 pence, or 1.3% to 261. Deutsche Bank lowered its recommendation for Britain’s largest retailer to “sell” from “hold” and downgraded shares of Next Plc to “hold” from “buy,” citing weak consumer demand which it expects to last through 2010. Rightmove Plc rallied 17.5 pence, or 8.4%,to 225 after the owner of the U.K.’s largest residential-property Web site reported a 29 percent gain in second-half profit, on higher advertising sales.

Currency –2.2406 Brambles PLC fell 14.75p or 6.61% to 2.0825 . Aussie Equiv A$4.67 Vol 30,660 – 1.00% Premium to Aussie close of $4.62 High – 2.1875(A$4.901) and low 2.07($4.638) Major Events

Monday, 2 March 2009 ECONOMICS Period GSJBW Mkt Prev Australia TD-MI Inflation Gauge Business Inventories Q4 +1.2% Inventories Contribution to GDP Company Gross Profits Q4 -5.0% United States Personal Income Jan n/a Personal Spending Jan n/a PCE Core Prices Jan (m/m) ISM Manufacturing Feb n/a Construction Spending Jan (m/m) EX-DIVIDEND (1.8624 points) AEF Goldman Sachs JBWere Overseas Wrap

US Bond Market Economic News

• Australia January Private Sector Credit +0.60% m/m and +6.10% y/y - higher than expected.

Consensus +0.30% m/m and +6/0% y/y. Previous -0.20% m/m (revised up from -0.30% m/m) and +6.50% y/y (revised down from +6.70% y/y).

• Japan January Industrial Production -10.0% m/m and -30.8% y/y - in line with expectations.

Consensus -10.0% m/m and -30.7% y/y. Previous -9.8% m/m and -20.8% y/y.

• Japan January Construction Orders -38.30% y/y. Previous -27.30% y/y. • Japan January Vehicle Production -41.0% y/y. Previous -25.20% y/y. • Japan January Housing Starts -18.70% y/y - lower than expected. Consensus -14.90% y/y. Previous -

5.80% y/y. Annualized Housing Starts 0.957M - lower than expected. Consensus 0.997M. Previous 1.001M.

• Japan February Nomura/JMMA Manufacturing PMI 31.6. Previous 29.6. • Japan January Jobless Rate 4.10% - lower than expected. Consensus 4.60%. Previous 4.30%

(revised down from 4.40%). Job-To-Applicant Ratio 0.67 - lower than expected. Consensus 0.69. Previous 0.73 (revised up from 0.72).

• Japan January Household Spending -5.90% y/y - lower than expected. Consensus -5.50% y/y. Goldman Sachs JBWere Overseas Wrap

• Japan February Tokyo CPI +0.50% y/y - higher than expected. Consensus +0.30% y/y. Previous

+0.50% y/y. Tokyo CPI Ex-Fresh Food +0.60% y/y - higher than expected. Consensus +0.30% y/y. Previous +0.50% y/y. Tokyo CPI Ex Food, Energy -0.10% y/y - higher than expected. Consensus - 0.30% y/y. Previous -0.30% y/y.

• Japan January Natl CPI 0.0% y/y - in line with expectation. Consensus 0.0%. Previous +0.40% y/y. Natl CPI Ex-Fresh Food 0.0% y/y - higher than expected. Consensus -0.10% y/y. Previous +0.20% y/y. Natl CPI Ex Food, Energy -0.20% y/y - in line with expectation. Consensus -0.20% y/y. Previous 0.0%.

• Japan January Retail Trade +0.60% m/m and -2.40% y/y - higher than expected. Consensus -0.50%

m/m and -3.0% y/y. Previous -1.90% m/m (revised up from -2.0% m/m) and -2.70% y/y. Large Retailers' Sales -5.60% m/m - higher than expected. Consensus -5.70%. Previous -6.20% m/m (revised up from - 6.30%).

• FT: RBS to sell Asian retail and banking assets. As part of its restructuring RBS plans to scale back its

operations in Asia, where its presence greatly expanded after the acquisition of ABN Amro. The bank had signalled its retreat from the region last month with the sale of its $2.4bn stake in Bank of China. Stephen Hester, RBS chief executive, went a step further on Thursday, announcing the sale of its Asian retail and commercial banking operations. It has hired Morgan Stanley to lead the divestment.

• Indonesia Sells Dollar Bonds Yielding Over 10 Percent. Indonesia, Southeast Asia’s biggest economy,

sold $3 billion of bonds in the largest dollar debt fundraising by a developing nation this year after offering more than double the premium over U.S. Treasuries it paid in June. Indonesia sold $2 billion of 10-year notes to yield 11.75 percent, or 8.759 percentage points more than similar-maturity U.S. Treasuries, according to Barclays Plc, which along with UBS AG arranged the sale. It also sold $1 billion of five-year notes to yield 10.5 percent, 8.474 points above U.S. government debt.

EUROPE • World Bank Press Release: EBRD, EIB and World Bank Group join forces to support Eastern Europe. The largest multilateral investors and lenders in Eastern Europe - the EBRD, the EIB Group, and the World Bank Group - have pledged to provide up to €24.5 billion to support the banking sectors in the region and to fund lending to businesses hit by the global economic crisis. This initiative complements national crisis responses and will deploy rapid, large-scale and coordinated financial assistance from the International Financial Institutions to support lending to the real economy through private banking groups, in particular to small and medium-sized enterprises. The financial support will include equity and debt finance, credit lines, and political risk insurance. The response takes into account the different macroeconomic circumstances in and financial pressures on countries in Eastern Europe, acknowledging the diversity of challenges stemming from the global financial retrenchment.

• Euro-Zone January Unemployment Rate 8.20% - higher than expected. Consensus 8.10%. Previous

• Euro-Zone January CPI -0.80% m/m and +1.10% y/y - in line with expectation. Consensus -0.80% q/q

and +1.10% y/y. Previous -0.10% q/q and +1.60% y/y. CPI - Core +6.10% y/y - lower than expected. Consensus +1.80% y/y. Previous +1.80% y/y.

• Germany February CPI +0.60% m/m and +1.0% y/y - higher than expected. Consensus +0.30% m/m

and +0.80% y/y. Previous -0.50% m/m and +0.90% y/y. CPI - EU Harmonised +0.70% m/m and +1.0% y/y - higher than expected. Consensus +0.30% m/m and +0.70% y/y. Previous -0.60% m/m and +0.90% y/y.

• Italy February Retailers' Confidence General 94.7. Previous 95.3 (revised down from 95.5). • Italy February Services Survey -32. Previous -30. • Italy December Large Company Empl. -0.70% y/y. Previous -1.0% y/y. • UK February GfK Consumer Confidence Survey -35 - higher than expected. Consensus -39.

• Lloyds Falls After Failing to Announce Asset Insurance Deal. Lloyds Banking Group Plc, the U.K.

bank that took over HBOS Plc last month, fell as much as 13 percent after saying it hasn’t reached agreement on a government asset insurance program. Talks with the U.K. Treasury are “progressing and well advanced,” the bank said in a statement today. The Treasury said it won’t make an announcement today.

• Darling Forces RBS to Give Up U.K. Tax Relief on Loss. Chancellor of the Exchequer Alistair Darling

forced Royal Bank of Scotland Group Plc to give up the right to claim its current losses against future taxes in the U.K., a potential boost to the Treasury’s finances. In exchange for guaranteeing 325 billion pounds ($462 billion) of RBS assets, the Treasury required the bank to forgo unspecified allowances that normally could be used to reduce its payments and also the right to count losses against taxes owed. The decision will help Prime Minister Gordon Brown confront the biggest budget deficits since modern records began in 1970 as the recession dries up revenue to the Treasury. RBS paid 16 billion pounds of corporate tax from 1998 to 2007, about 80 percent of the cost of its government-funded recapitalization.

• Norway Q4 Manufacturing Wage Index +1.0% q/q. Previous +2.50% q/q. Goldman Sachs JBWere Overseas Wrap

• Sweden Q4 GDP -2.40% q/q and -4.90% y/y - lower than expected. Consensus -1.60% q/q and -2.10%

y/y. Previous -1.0% q/q (revised down from -0.10% q/q) and -0.10% y/y (revised down from 0.0% y/y).

• Sweden January Retail Sales +1.30% m/m and +2.20% y/y - higher than expected. Consensus -

0.50% m/m and -0.40% y/y. Previous -0.10% m/m and -1.10% y/y.

• Sweden Q4 Current Account Surplus SEK 63.6B. Previous Surplus SEK 70.9B (revised up from SEK

• Sweden January PPI +0.90% m/m and +3.90% y/y - higher than expected. Consensus +0.40% m/m

and +3.0% y/y. Previous -0.80% m/m (revised down from -0.70% m/m) and +4.60% y/y (revised up from +3.80% y/y).

• Switzerland February KOF Swiss Leading Indicator -1.41 - lower than expected. Consensus -0.93.

Previous -0.93 (revised down from -0.87).

• Hungary Seeks $230 Billion Package for Eastern Europe. Hungarian Prime Minister Ferenc

Gyurcsany wants the European Union to arrange a package of as much as 180 billion euros ($230 billion) to help east European economies, banks and companies weather the financial crisis. A “European Stabilization and Integration Program” would include short-term financing for governments, coordinated restructuring for private debt, the recapitalization of banks and liquidity for companies in as many as 12 countries, Gyurcsany, 47, said in an interview in Budapest yesterday. He will present the plan at a March 1 EU summit in Brussels.

• FT: Iceland looks to restructure $3.6bn of debt. Iceland’s new government is working on a plan to

restructure billions of dollars of its bonds held by foreign investors as part of a drive to restore confidence in its shattered economy. Foreign investors own up to ISK400bn ($3.6bn, €2.8bn, £2.5bn) in krona-denominated bonds which the central bank fears could be dumped once capital controls imposed during its banking crisis are removed. The Icelandic central bank has warned a huge outflow of currency would seriously destabilise the krona and these fears are one of the main reasons the capital controls are still in place.

Goldman Sachs JBWere Overseas Wrap

Currency

This communication may be confidential and is not intended to be used by anyone other than the recipient. Goldman Sachs JBWere Pty Ltd and its affiliates (GSJBW) reserves the right to intercept and monitor the content of e-mail messages to and from its systems. This communication is not an offer or solicitation to buy or sell any security. This document contains general information only. In preparing this communication, GSJBW did not take into account the investment objectives, financial situation and particular needs ('financial circumstances') of any particular person. Accordingly, before acting on any advice contained in this communication, you should assess whether the advice is appropriate in light of your own financial circumstances or contact your GSJBW adviser. Opinions expressed are current opinions only. Opinions, historical price(s) or value(s) are as of the date and, if applicable, time, indicated. Goldman Sachs JBWere Pty Ltd and its affiliates distributing this communication and each of their respective directors, officers and agents ("GSJBW Group") Goldman Sachs JBWere Overseas Wrap believe that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations contained in this communication are reasonably held or made as at the time of compilation. However, no warranty is made as to the accuracy or reliability of any estimates, opinions, conclusions, recommendations (which may change without notice) or other information contained in this document and, to the maximum extent permitted by law, GSJBW Group disclaims all liability and responsibility for any direct or indirect loss or damage which may be suffered by any recipient through relying on anything contained in or omitted from this communication. This material is not for distribution in the United Kingdom to private customers, as that term is defined under the rules of the Financial Services Authority. Further information on any of the securities mentioned in this material may be obtained on request. Copyright 2003 Goldman Sachs JBWere Pty Ltd and its affiliates distributing this document. All rights reserved. NOTICE TO RECIPIENT: This communication is not intended for U.S. recipients and you should not forward this material into the United States or to any U.S. persons.

ASTRON LIMITED (ATR) – RTL( A) Goldman Sachs JBWere and/or its affiliates is acting as financial advisor to Astron Limited in its consideration of strategic options, including consideration of an approach by a third party in relation to a possible transaction involving the sale of its zirconia materials business based in China. Goldman Sachs JBWere and/or its affiliates may receive a fee for acting in this capacity. BHP BILLITON LIMITED AND RIO TINTO LIMITED - RTL(R) Goldman Sachs JBWere is currently acting as Financial Advisor to BHP Billiton and as such is an associate of BHP Billiton for the purpose of the Takeover Code. Goldman Sachs JBWere and/or its affiliates may receive a fee for acting in this capacity. BLUESCOPE STEEL LIMITED (BSL) – RTL( A) Goldman Sachs & Co., is acting as financial advisor to Ternium SA in relation to the stock purchase agreement of its subsidiary IMSA Acero, S.A. de C.V., with BlueScope Steel North America Corporation. Goldman Sachs & Co., may receive a fee for this advisory role. COATES HIRE LIMITED - RTL(A) AND NATIONAL HIRE LIMITED - RTL(A) Goldman Sachs JBWere Pty Ltd and / or its affiliates is acting as both a financial advisor and financier to the Ned Group Consortium (which comprises National Hire Limited and Carlyle Group) in connection with its proposed acquisition of Coates Hire Limited. Goldman Sachs JBWere and / or its affiliates may receive a fee(s) for acting in these capacities. HEALTHSCOPE LIMITED – RTL( A) AND SYMBION LIMITED- RTL(A) Goldman Sachs JBWere and/or its affiliates is acting as financial advisor to Healthscope Limited in connection with Symbion Health Limited. Goldman Sachs JBWere and/or its affiliates may receive a fee for its financial advisory role. MEDIBANK PRIVATE LIMITED (unlisted) Goldman Sachs JBWere and/or its affiliates has been appointed as Joint Lead Manager to the potential initial public offering of securities in Medibank Private Limited. Goldman Sachs JBWere and/or its affiliates may receive fees for acting in this capacity NORFOLK GROUP LIMITED – RTL (R) Goldman Sachs JBWere and/or its affiliates are a substantial shareholder in the company or trust. JBWere (NZ) Private Equity Limited, a member of the Goldman Sachs JBWere Group, is investment manager of, and holds shares in various entities that comprise Hauraki Fund. Hauraki Fund holds shares in Norfolk. Those shares held by JBWere (NZ) Private Equity Limited confer on it, and entities associated with certain Goldman Sachs JBWere Group employees, a right to share in distributions made by Hauraki Fund, subject to preferential entitlements of other investors in Hauraki Fund. A director or employee of Goldman Sachs JBWere and/or its affiliates is a director of the company. Goldman Sachs JBWere and/or its affiliates has managed or co-managed a public offering of securities of the company or its affiliates in the past 12 months. NEWS CORPORATION (NWS) - RTL (A) Goldman Sachs is acting as financial advisor to News Corp in an announced strategic transaction. THE WAREHOUSE GROUP LIMITED (WHS) - RTL(A) Goldman Sachs JBWere Pty Ltd and/or its affiliates is acting as financial advisor to a consortium in relation to the proposed acquisition of the shares or assets of The Warehouse Group Limited. Goldman Sachs JBWere will receive a fee(s) for acting in this capacity VECTOR LIMITED (VCT.NZ) - RTL(A) Goldman Sachs JBWere and/or its affiliates is acting as financial advisor to Vector Limited with regard to strategic issues and options for their Wellington electricity business. Goldman Sachs JBWere and/or its affiliates will receive a fee for its financial advisor role. ____________________________________________________________________________ 2. The following companies ONLY require the FA disclosure

AUSTRALIAN STOCK EXCHANGE LIMITED (ASX) Goldman Sachs JBWere Pty Ltd, along with New Zealand Exchange Limited (NZX) and certain other brokers in Australia, is a shareholder in a company intending to launch a new Australian ECN (Electronic Communications Network) to initially deliver a new securities reporting platform to market participants. NEW ZEALAND EXCHANGE LIMITED (NZX.NZ) Goldman Sachs JBWere Pty Ltd, along with New Zealand Exchange Limited (NZX) and certain other brokers in Australia, is a shareholder in a company intending to launch a new Australian ECN (Electronic Communications Network) to initially deliver a new securities reporting platform to market participants.

REV ARGENT NEUROC | VOL. 27, Nº 4 : S020-S038 | 2013 RESúMENES Resúmenes de los Trabajos Presentados en TRABAJOS DE PRESENTACIÓN ORAL VASCULAR Marcos Daniel Chiarullo, Juan Manuel Lafata, Marcelo Orellana, Jorge Bustamante, Pablo Rubino, Jorge Lambre. Servicio de Neurocirugía. Hospital Alta Complejidad En Red COILS/CLIP, ISAT vs BRAT. Revisión Bibliográfica “El Cruc

HEALTHY STUDENTS, ENGAGED LEARNERS WORKSHOP SCHEDULE 9:00 am – Keynote Speaker: Ron Morrish on The Teenage Brain Whether you already have a teen or soon will, Ron will help you understand the neurological changes in the mysterious teenage brain. For parents/guardians, teenagers can be hard to fathom. If you find yourself asking, “why on earth did you do that” on a regular bas

Goldman Sachs JBWere

Goldman Sachs JBWere

Goldman Sachs JBWere

Goldman Sachs JBWere